levelUP Financial Wellness®

Get Started

Empowering everyone to make smarter financial decisions and live better.

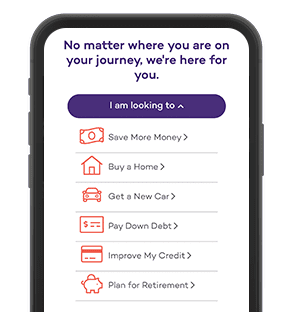

Ready to take your finances to the next level? Our levelUP Financial Wellness®

program helps improve your money management skills with the tools and advice you need to reach your financial goals. We've empowered more than 1,000 local students and 10,000 MECU members with the confidence they need to make better financial decisions. Get started on a plan today!

Meet with a levelUP Financial Counselor

Access one-on-one financial counseling with a personalized plan and expert guidance along the way. 100% complimentary for MECU members.

Attend a levelUP live workshop near you

Our free interactive workshops cover popular financial topics in an informal classroom setting. View upcoming events.

levelUP for Employers

Leading Baltimore-area companies partner with MECU to provide credit union membership to their employees and their families. We work with companies of all sizes. Learn More >

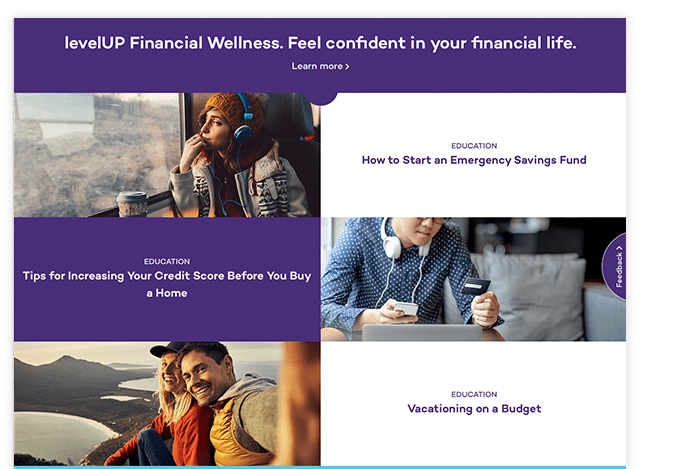

levelUP Online

Free 24/7 resources to equip you with the knowledge and skills you need to make the financial decision that are best for you. Choose a playlist below that best matches your interest area.